Why Timing Changes Everything in Cultural Inheritance – A Real Approach

Inheriting family assets isn’t just about money—it’s tied to traditions, values, and sometimes, complicated emotions. I’ve seen heirs lose more than wealth simply because they acted too soon or waited too long. The real game-changer? Timing. When you transfer, accept, or manage culturally significant assets can impact both financial outcomes and family harmony. This is how smart timing transforms cultural inheritance from a burden into a legacy.

The Hidden Weight of Cultural Inheritance

Cultural inheritance encompasses far more than property deeds or bank accounts. It includes ancestral land, family-run businesses, sacred artifacts, traditional crafts, and even the intangible values embedded in how a family lives, celebrates, and remembers. These assets are not merely financial—they are vessels of identity, continuity, and belonging. Unlike standard estate planning, where the focus is on asset distribution and tax efficiency, cultural inheritance operates on a deeper level. It involves emotional attachments, generational expectations, and often, unwritten rules about who should inherit what and when. This complexity makes timing not just a logistical detail, but a central factor in preserving both wealth and unity.

For many families, especially those with roots in collectivist cultures, the transfer of cultural assets is governed by tradition rather than legal frameworks. A piece of farmland passed down for generations may carry the memory of ancestors who tilled it; a family-owned shop may represent decades of sacrifice and community trust. These meanings cannot be quantified on a balance sheet, yet they influence decisions profoundly. When heirs receive such assets without proper context or preparation, the result can be a loss of both value and meaning. The land may be sold too cheaply, the business mismanaged, or the artifact stored improperly—eroding both financial and cultural capital.

Moreover, cultural inheritance often involves multiple stakeholders, including extended family members, religious institutions, or even entire communities. In some cultures, the eldest son is expected to inherit leadership of the family enterprise, while daughters receive other forms of support. In others, land is held collectively and cannot be divided. These customs, while meaningful, can create tension when modern realities—such as urbanization, migration, or changing gender roles—challenge traditional norms. Timing becomes critical in navigating these shifts. Transferring assets too early may disrupt established hierarchies; delaying too long may leave heirs unprepared to uphold responsibilities. The challenge lies in honoring tradition while adapting to change—something that requires careful, intentional timing.

Why Timing Is the Silent Decider in Inheritance Success

The moment an inheritance is transferred can quietly determine its long-term success or failure. While many families focus on the legal and financial mechanics of estate planning, they often overlook the strategic importance of timing. A well-drafted will and a solid trust structure are essential, but they cannot compensate for a poorly timed transfer. The difference between a smooth transition and a costly dispute often comes down to when the handover occurs—not just in calendar terms, but in alignment with economic conditions, family readiness, and legal frameworks.

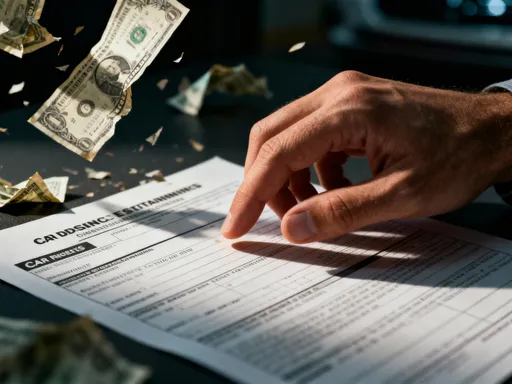

Financially, timing affects everything from tax liabilities to market valuation. Receiving an asset during a market downturn may mean accepting a lower valuation, potentially leading to underpayment of taxes or missed opportunities for appreciation. Conversely, transferring property at the peak of a real estate boom could trigger higher capital gains taxes or attract unwanted scrutiny from tax authorities. In cross-border inheritances, timing also interacts with international tax treaties and currency fluctuations. For example, transferring ownership of a vacation home in another country just before a currency devaluation could significantly alter the asset’s real value. These are not hypothetical concerns—they are real risks that families face when timing is treated as an afterthought.

Equally important is the readiness of the next generation. A family business passed to a 25-year-old who lacks experience in management, finance, or operations is at high risk of decline. Studies have shown that less than 30% of family businesses survive into the third generation, and poor timing in leadership transitions is a major contributing factor. The transfer of control should align with the heir’s personal and professional development. This means not just age, but also demonstrated competence, emotional maturity, and commitment to the family’s values. Rushing the process can lead to mismanagement; delaying it can stifle innovation and create resentment among younger members eager to contribute.

Legal compliance is another area where timing plays a decisive role. In many jurisdictions, inheritance laws require certain procedures—such as probate, notarization, or public registration—to be completed within specific timeframes. Missing these windows can result in penalties, loss of ownership rights, or prolonged legal battles. In multicultural families, conflicting inheritance laws across countries can complicate matters further. For instance, a parent may intend to leave property to one child under the customs of their home country, but local laws in the country of residence may mandate equal distribution among all children. Addressing these issues in advance, and timing the transfer to align with legal requirements, can prevent costly disputes down the line.

The Cost of Waiting: Real Risks in Delayed Transfers

One of the most common—and most damaging—mistakes in cultural inheritance is waiting until a parent passes away to begin the transfer process. While this may seem respectful or natural, it often leads to avoidable complications. Procrastination can turn what should be a structured transition into a crisis management scenario. When transfers are delayed until after death, families lose the opportunity to clarify intentions, resolve disagreements, and ensure that heirs understand the full context of what they are receiving. The absence of the parent—the central figure in the family’s story—can leave critical questions unanswered and decisions clouded by grief.

A major consequence of delayed transfers is the loss of knowledge. Cultural assets often come with stories, traditions, and practical know-how that are not written down. The parent may know the history of a piece of land, the origin of a family heirloom, or the unwritten rules of running a traditional business. When these details are not passed on during their lifetime, they risk being lost forever. An heir may inherit a valuable artifact but not know its significance, leading to improper storage or even accidental disposal. A family recipe book may be passed down, but without the oral instructions on technique or timing, its value diminishes. This erosion of cultural context can be just as damaging as financial loss.

From a legal and financial standpoint, posthumous transfers are often more complex and costly. Probate—the legal process of validating a will and distributing assets—can take months or even years, during which time assets may lose value or generate disputes among heirs. In some cases, the lack of updated documentation can make it difficult to prove ownership, especially for older properties or businesses with informal records. This is particularly true in rural or developing regions where land titles may not be formally registered. Heirs may discover that property rights have weakened over time due to boundary disputes, encroachments, or changes in land use regulations. What was intended as a gift becomes a legal burden.

Tax implications also become harder to manage after death. In many countries, inheritance taxes are calculated based on the value of the estate at the time of death, which may be higher than during the parent’s lifetime due to market appreciation. Without prior planning, families may face unexpected tax bills that force the sale of assets to cover liabilities. In some cases, heirs may be unable to afford the taxes and lose the property altogether. These outcomes are preventable with timely planning, yet they occur regularly because families wait too long to act.

Acting Too Soon: The Perils of Premature Handover

While delaying inheritance carries risks, rushing the process can be equally harmful. Transferring control of assets before the next generation is ready often leads to financial loss, family conflict, and the erosion of cultural values. The intention may be noble—to empower young heirs, reduce future tax burdens, or ensure continuity—but without proper preparation, early transfers can backfire. The key is not speed, but alignment between the asset, the recipient, and the moment.

One of the most common pitfalls is transferring financial control to heirs who lack experience in money management. A young adult who has never budgeted, invested, or run a business may struggle to handle a sudden influx of wealth. Without guidance, they may make impulsive decisions—such as overspending, taking on excessive debt, or making risky investments—that deplete the asset base. In family businesses, premature leadership can lead to poor strategic choices, employee turnover, and customer loss. A case study from a global family business advisory group found that 40% of early-succession attempts failed within five years due to lack of preparation and oversight.

Emotional readiness is just as important as financial competence. Inheritance is not just a transaction—it is a rite of passage that carries psychological weight. Receiving control of a family business or ancestral home too early can create pressure, anxiety, and identity conflicts. The heir may feel overwhelmed by expectations or struggle to assert authority over older relatives or long-time employees. At the same time, the parent who steps aside too soon may experience a loss of purpose or feel excluded from decisions, leading to resentment. These emotional dynamics can destabilize family relationships and undermine the very unity that cultural inheritance is meant to preserve.

From a legal perspective, reversing a premature transfer is often difficult and expensive. Once property is deeded or shares are transferred, reclaiming control typically requires legal action, which can be time-consuming and damaging to family trust. In some jurisdictions, early transfers may also trigger immediate tax liabilities, such as gift taxes or capital gains, that could have been deferred with better timing. Additionally, transferring assets before the parent has secured their own financial future can leave them vulnerable in old age, especially if healthcare costs rise unexpectedly. A balanced approach—where the parent retains sufficient resources while gradually preparing the heir—is far safer and more sustainable.

Strategic Windows: When to Transfer, Accept, or Hold

Successful cultural inheritance is not about reacting to events—it is about creating strategic timing windows through deliberate planning. These windows are moments when financial, emotional, and legal factors align to support a smooth and meaningful transfer. They do not happen by chance; they are the result of foresight, communication, and preparation. Families that master this approach treat inheritance not as a single event, but as a process that unfolds over years, even decades.

One effective strategy is phased transfer, where responsibilities and assets are handed over gradually. For example, a parent might begin by involving the heir in business meetings, then assign them to manage a division, and finally transfer full ownership when they demonstrate consistent performance. This approach allows the heir to gain experience, build confidence, and earn the respect of employees and partners. In real estate, phased transfer might involve co-ownership arrangements or lease agreements that give the heir control while the parent retains a life estate. This ensures continuity without sacrificing the parent’s security.

Life milestones also provide natural timing opportunities. Marriage, the birth of a first child, retirement, or a significant birthday can serve as symbolic and practical transition points. These events often prompt reflection on legacy and responsibility, making them ideal moments to discuss and implement inheritance plans. For example, a parent might choose to transfer a family home to their child upon the birth of their first grandchild, framing it as a gift to the next generation. Such moments carry emotional resonance that can strengthen family bonds and reinforce cultural values.

Market and regulatory conditions also create strategic windows. A period of low interest rates may be ideal for refinancing family property or restructuring debt. Upcoming changes in tax law—such as adjustments to inheritance or capital gains tax rates—can prompt timely transfers to preserve value. For instance, transferring assets before a new tax rule takes effect can result in significant savings. Similarly, transferring ownership during a market downturn may allow heirs to acquire assets at a lower valuation, reducing future tax liabilities. These decisions require close monitoring of economic trends and professional advice, but the benefits can be substantial.

Tools and Tactics for Smarter Timing Decisions

Families do not have to navigate the complexities of cultural inheritance alone. A range of legal, financial, and communication tools can help them make smarter timing decisions. These tools do not eliminate risk, but they provide structure, clarity, and protection—replacing emotional hesitation with informed action.

Trusts are among the most powerful instruments for controlling timing. A well-structured trust allows the grantor to specify when and how assets are distributed, based on age, achievement, or life events. For example, a trust might release funds when an heir turns 30, graduates from university, or starts a business. This prevents premature access while ensuring that support is available when needed. Trusts also offer privacy, tax advantages, and protection from creditors—making them ideal for preserving both financial and cultural wealth.

Family constitutions—formal documents that outline values, governance rules, and inheritance principles—help align expectations across generations. They provide a shared reference point for decision-making and reduce ambiguity in emotionally charged situations. A constitution might specify that leadership of a family business rotates among siblings, or that ancestral land must remain in the family for at least 50 more years. While not legally binding in all jurisdictions, these documents carry moral authority and can prevent disputes by clarifying intentions in advance.

Regular family meetings are another essential tool. These gatherings create space for open dialogue, education, and conflict resolution. They allow parents to share their vision, heirs to ask questions, and advisors to provide updates. When conducted consistently, family meetings build trust and prepare the next generation for their roles. Some families even establish family councils or advisory boards to oversee major decisions, ensuring that no single person holds unchecked power.

Professional advisors—such as estate planners, tax specialists, and cultural consultants—bring objectivity and expertise to the process. They can help families navigate complex regulations, assess risks, and design customized strategies. Technology also plays a growing role. Digital archives can preserve family histories, photos, and business records, ensuring that cultural context is not lost. Secure platforms allow families to share documents, track asset performance, and coordinate decisions across distances. Together, these tools empower families to take control of timing, rather than being controlled by it.

Turning Timing into Legacy: A Balanced Path Forward

Ultimately, the goal of cultural inheritance is not just to pass on assets, but to pass on meaning. Timing is the thread that weaves together financial prudence, emotional intelligence, and cultural continuity. When managed wisely, it transforms inheritance from a transaction into a legacy—a living connection between past, present, and future. The most successful families understand that timing is not about waiting for the perfect moment, but about creating the right conditions for a successful transition.

This balanced approach requires patience, communication, and planning. It means respecting tradition without being bound by it, preparing heirs without rushing them, and using tools without losing sight of values. It means recognizing that a family’s wealth is not just measured in money, but in the strength of its relationships, the depth of its heritage, and the resilience of its future. By aligning timing with purpose, families can ensure that their cultural inheritance does not become a source of conflict or loss, but a foundation for growth, unity, and enduring significance.

In a world of rapid change, cultural inheritance offers stability, identity, and belonging. But it only endures when handled with care, wisdom, and the right timing. The choices made today—about when to transfer, when to hold, and when to guide—will shape the legacy for generations to come. With thoughtful planning, cultural inheritance becomes more than a gift. It becomes a bridge—connecting the values of the past to the possibilities of the future.